Tax Reform Impact on Real Estate Professionals

National Association of REALTORS® VP David Greer recently held a video chat with NAR Senior Legislative Policy Representative Evan Liddiard and Business Planning Group Owner Peter Baker to see how the law affects your taxes as a business. Below are some highlights; click here to view the full 43-minute video.

DISCLAIMER: In accordance with certain professional standards, this webcast/transcription is not written tax advice directed at the particular facts and circumstances of any person. This webcast is not intended to contain tax advice; any material or discussions contained in, forwarded with, or related to this webcast is not intended by NAR or Peter Baker to be used, and cannot be used, by any person as a substitute for obtaining their own tax planning in consultation with independent tax advisor, or for the purpose of avoiding penalties that may be imposed under the Internal Revenue Code.

GREER: Our members are independent contractors and sole proprietors and they report their income on 1099s. How does the law impact our members?

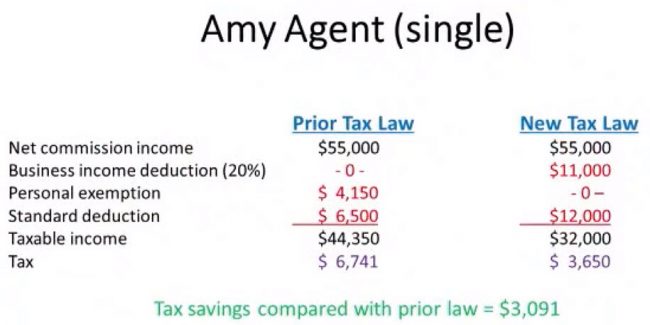

LIDDIARD: There’s a 20-percent deduction available on qualified business income. Let’s start with a simple example of someone we’ll call “Amy Agent”. Let’s assume that Amy has net commission income for 2018 at $55,000. That would be net income and you’ll see that under the current law, there was no such deduction. This is a brand new deduction of 20 percent. She would get to take $11,000 right off the top. In addition, she can deduct a standard deduction.

Now, under the prior law, that was $4,150; that has been repealed. No longer is it available, but the standard deduction has gone up to $12,000. Personal exemption is gone. Standard deduction is up to $12,000. The taxable income has gone down quite a bit and she gets a tax cut of about $3,100 compared to the current law , much of it attributable to this new business income deduction because she’s in business for herself.

Married, Filing Jointly

GREER: How about those who are married and filing jointly?

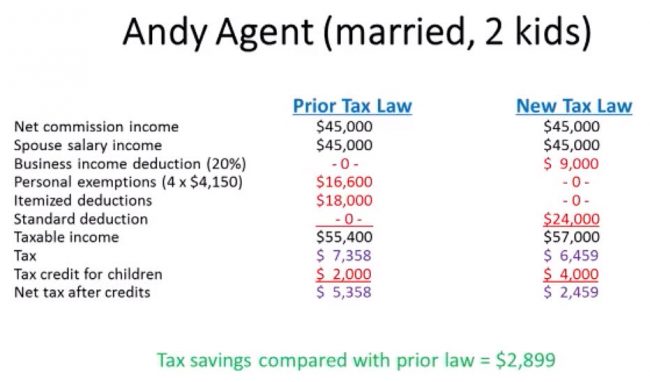

LIDDIARD: This is where it gets a little bit more complicated…[look at] “Andy Agent” who is married with a couple of kids. The spouse of Andy also has a salary income, so under the prior law, they had each $45,000 of income — Andy through his commission income and Andy’s spouse through salary income. No deduction under the prior law, but 20 percent of Andy’s commission income is applicable to this deduction, or $9,000.

Andy also loses the personal exemptions. In this case, they’ve got a couple of kids, so it’s a big hit, but they get a much higher standard deduction. There’s a big deduction here that’s going to make a difference. In this case, Andy and his family are going to get a tax cut of about $2,900. Much of it attributable again to this business income deduction.

Non-Personal Service Income

GREER: What exactly is considered non-personal service income?

LIDDIARD: This comes down to the question of whether somebody is in business for themselves, and is earning income from that business. Now, both personal service income and non-personal service income are eligible, but it becomes an important issue when they start getting to the income levels where this phases out.

Essentially, personal service income is income earned by your own expertise. Me as an accountant…real estate agents, because they are in business to share their expertise about real estate. That’s what they’re selling, that’s what they’re being compensated for; that’s their personal income.

Agent Expertise vs. Broker

GREER: Is there a difference between say agents and their expertise, and say, brokers?

LIDDIARD: There could be, yes, because a broker is going to get part of his or her income, because of that expertise as well, that know-how, but they may also get income because they’ve got an established business with a building…equipment…intangibles, such as a name brand and so forth that’s well known.

To that extent, they’re getting compensated for their investment in the business. Again, this becomes important when you get to the higher levels. For our audience, it’s important to know that this deduction begins to phase out for a married couple filing jointly at $315,000. For a single person, it’s half that, $157,500.

There’s a phase out range and then it’s gone, but if you’re receiving your income from non-personal service income, then there’s an exception that allows you to get a partial or full deduction, depending on how much wage income you paid and how much you have invested in your business.

BAKER: Often, the broker’s ownership interest in the real estate organization he’s running comes to him through a K-1, a pass-through entity — whether it’s an S corporation, an LLC, or a partnership.

This concept of the 20 percent business deduction is really a broad spectrum of both sole proprietors and pass-through entities including S corporations, LLCs, and partnerships.

There might be multiple streams in which a taxpayer then has income flowing to them and each of those streams really are measured in terms of this threshold that Evan (Liddiard) described.

Related Appendix:

Examples of How the Deduction for Qualified Business Income May Affect Various Real Estate Professionals Tags: Amy Agent, Andy Agent, commission income, David Greer, Evan Liddiard, non-personal service income, personal exemption, personal service income, Peter Baker, tax deductions, tax reform